Banks and mortgage interest (III)

Banks and mortgage interest (III)

Coincidence or not, but from 2009 the development of mortgage interest rates in the Netherlands will continue to differ from those in the rest of Europe. About the how and why has since been discussed. In fact, there is an oligopoly in the Netherlands, causing competition; there is virtually no identifying factors that justify higher interest, such as higher costs. It goes without saying that banks insist on the higher costs.

Rabobank does that too. In a brief comment on a report by the Dutch Competition Authority from November 2010, Rabobank acknowledges that the margins on the new mortgages have improved since mid-2009. However, the bank adds, the costs for the mortgages have also gone up.

Rabobank calls the remaining margin healthy and necessary to be able to do so grant mortgages under the new Basel III regulations. The margin is needed to cover operating costs and profit is needed to strengthen equity.

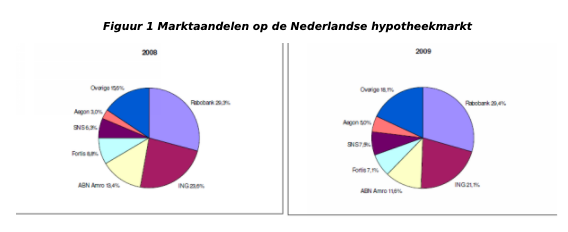

Figure 1: Market shares in the Dutch mortgage market

All things considered, Rabobank's comments do make some sense. As in 2009, the first contours of the Basel III agreement become visible.

Although the Basel II Capital Accord for banks was only introduced in 2008, the crisis has caused the limitations of that accord exposed. The Basel Committee announced that from 2009, banking supervision will be working on proposals to regulate the capital requirements for banks worldwide.

These proposals were contained in two consultation documents. According to DNB, the impacts of Basel III are great for Dutch banks when it comes to capital and liquidity. She recommends the banks to think carefully about the retention of profits and about adjusting the fund profiles, as stated in the 2010 annual report.

A year later, it was concluded that Dutch banks are successfully working on strengthening their own capital buffers. At the end of 2011, these amount to 11.9% against 9.3% in 2008 when it comes to risk-weighted assets.

When it comes to the unweighted capital ratio, the leverage ratio, the picture is gloomier. The Dutch banking sector ranked the least in Europe, according to DNB.

In the same breath, the Bank also notes that Dutch banks under Basel III have problems with long-term financing requirements. That mainly has to deal with the large mortgage portfolios representing the size of domestic deposits far exceed. There is a funding gap and banks are struggling to fill that gap. This is due to the precarious situation in the financing markets.

The suggestion is clear. Banks have to incur more costs to fill the financing gap. Higher mortgage interest is therefore justified, such as Rabobank states in its annual report. This certainly applies in light of the Basel III requirements. The problem for the banks and therefore also for Rabobank is, for example, a study by the Central Planning Bureau (CPB) from February cannot find confirmation for the claim that Dutch banks have to incur more costs for providing mortgages than their foreign counterparts. The CPB concludes that a lack of competition in combined with price leadership, a possible explanation for the higher mortgage interest.

The CPB does not want to go further as Dutch banks benefited from higher mortgage rates, which endorses Rabobank in its 2010 annual report. Whether the banks abused the situation? A definitive answer is not clear.

Banks do appear to be inventive to take optimal advantage of the given circumstances. In the 2009 annual report, BDB concluded that banks have higher regular loans net interest income. They benefited from the increased interest margin, the difference between the loan and loan rates.

The interest margin rose because banks did not fall in the sharply decreased ECB policy rate which was passed on to their borrowers. That decrease was translated into the savings interest.